Mandatory Climate Reporting – Reminder

Australia’s climate related financial reporting regime created by the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 (Cth) (Regime) took effect on 1 January 2025.

The Regime imposes mandatory climate related reporting obligations (as specified in AASB S2) on different categories (Groups) of reporting entities which are required to prepare financial reports under Chapter 2M of the Corporations Act 2001 (Cth) (for example, because they are a public company or a large proprietary company). Entities registered with the Australian Charities and Not-for-profits Commission are excluded from reporting under the Regime.

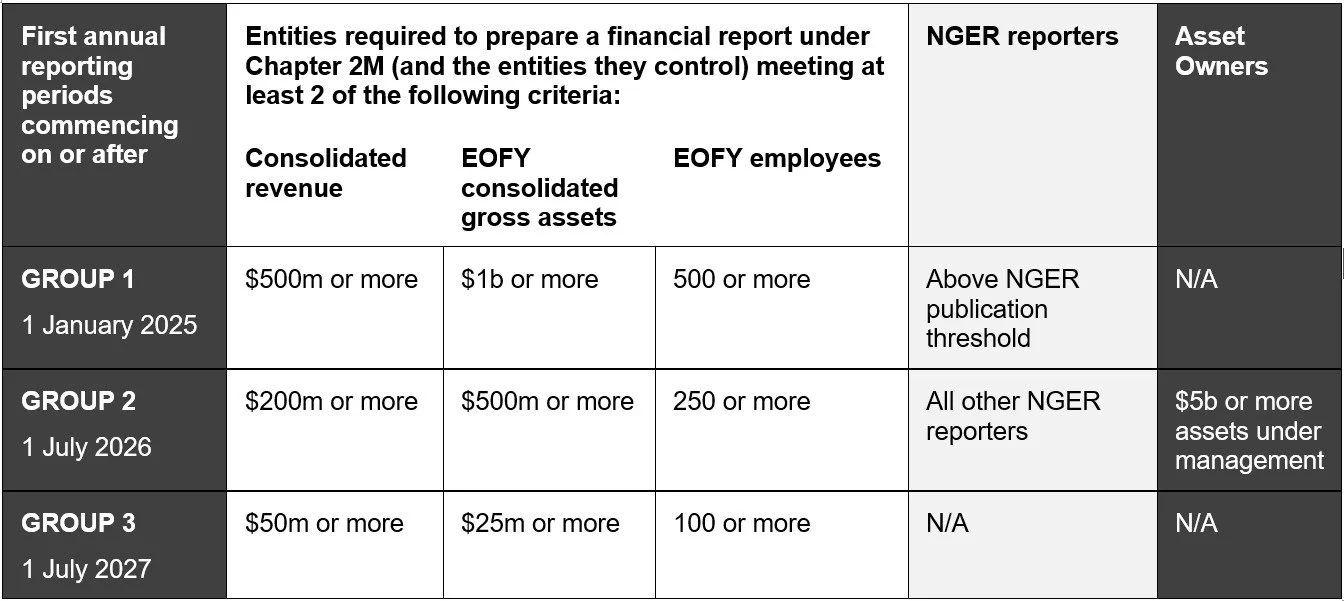

A staggered approach has been adopted for commencement of the new reporting obligations as specified in the table below, with Group 1 reporting entities already bound by the new regime for reporting periods commencing on or after 1 January 2025.

The relevant Groups included in the Regime, as identified in the table below are as follows:

Group 1: reporting entities (and the entities they control) which meet 2 of the 3 defined criteria specified below and NGER reporters (entities required to report under the National Greenhouse and Energy Reporting Act 2007 (Cth));

Group 2: reporting entities (and the entities they control) which meet 2 of the 3 defined criteria specified below, NGER reporters and asset owners (registered schemes, registrable superannuation entities and retail CCIVs where the EOFY assets of that owner and the entities they control exceeds $5b);

Group 3: all reporting entities (and the entities they control) which meet 2 of the 3 defined criteria specified below.

With the impending Federal election in 2025, eyes will be on both sides of politics to see how the Regime might change in the near future.

But this uncertainty should not stop Group 1 entities from taking the required action to achieve compliance right away and compliance with the voluntary AASB S1 will continue to be best practice for many entities regardless of how the Regime is impacted politically.

Group 2 and 3 entities can also take steps now to get ahead of the curve and in particular, to start understanding their climate-related risks and opportunities and to consider implementing systems and processes for the collection and management of climate-related information.